When you discover damage to your roof, one of the first questions that crosses your mind is whether you should involve your insurance company. The answer isn't always straightforward. Filing a claim can provide financial relief for major repairs, but it can also trigger premium increases and become part of your claims history. Understanding when to call your insurer and when to handle repairs independently helps you make a decision that protects both your home and your wallet. For homeowners across Eastern North Carolina dealing with coastal weather, knowing these guidelines matters even more.

Understanding What Your Insurance Actually Covers

Most homeowner policies cover sudden, unexpected damage from what insurers call "covered perils." These typically include wind, hail, fire, and falling objects like tree limbs. What they usually don't cover is gradual wear, aging materials, or lack of maintenance.

Common covered scenarios include:

- Storm damage from hurricanes or severe thunderstorms

- Hail impact that cracks or punctures shingles

- Wind that tears off sections of roofing

- Falling trees or large branches

- Fire or lightning strikes

Typically excluded situations:

- Normal aging and weathering over time

- Manufacturer defects in roofing materials

- Damage from neglected maintenance

- Pre-existing conditions that weren't addressed

- Cosmetic damage that doesn't affect function

The question of should i call insurance for roof damage becomes clearer when you understand this distinction. If a hurricane tears off part of your roof, that's clearly covered. If your 25-year-old shingles are simply worn out, that's your responsibility as the homeowner.

The Claims History Factor

Every claim you file becomes part of your insurance record through databases like CLUE (Comprehensive Loss Underwriting Exchange). Future insurers can see this history when you shop for coverage or even when you sell your home.

Filing multiple claims within a short period can lead to non-renewal or difficulty finding affordable coverage. Some insurers have specific thresholds, such as dropping coverage after two claims in three years. This makes the decision about whether to file more complex than simply comparing your deductible to the repair cost.

When You Should Definitely Call Your Insurance

Certain situations clearly warrant an insurance claim, regardless of other considerations. The damage is too extensive or expensive to handle out of pocket, and the long-term benefits outweigh the potential downsides.

Major Structural Damage

If a storm has compromised the structural integrity of your roof, you should file a claim immediately. This includes situations where:

- Large sections of roofing are missing or damaged

- The roof deck is exposed or compromised

- Water is actively entering your home

- There's visible sagging or structural deformation

Structural damage typically costs tens of thousands to repair or replace. These amounts far exceed what most homeowners can comfortably pay out of pocket, making a claim the practical choice.

Multiple Areas Affected

When damage spreads across various parts of your roof rather than one isolated spot, total repair costs escalate quickly. A storm that affects three or four roof planes, damages flashing around chimneys and vents, and impacts gutters represents significant expense.

According to Kin Insurance’s guidance on roof damage claims, homeowners should consider filing when damage is substantial enough that repair costs significantly exceed the deductible and when structural elements are weakened or compromised.

| Damage Extent | Typical Cost Range | File Claim? |

|---|---|---|

| Single missing shingle | $100-300 | Usually no |

| 10-15 damaged shingles | $500-1,500 | Maybe |

| Quarter of roof damaged | $3,000-8,000 | Likely yes |

| Majority of roof compromised | $8,000-25,000+ | Definitely yes |

Emergency Situations

If you're dealing with active leaks or exposure that threatens interior damage, don't wait to contact your insurer. Filing claims promptly protects you from potential denials based on delayed reporting and prevents additional damage that could complicate the claim.

When Paying Out of Pocket Makes More Sense

The decision about should i call insurance for roof damage often tilts toward handling repairs yourself when the numbers and circumstances align in specific ways.

Damage Below or Near Your Deductible

Most homeowner policies carry deductibles between $1,000 and $2,500, though some coastal policies have higher thresholds or percentage-based deductibles. If your repair estimate is $1,200 and your deductible is $1,000, you're only saving $200 by filing a claim.

Consider these calculations:

- Get a detailed repair estimate from a local contractor

- Subtract your deductible from the total cost

- Evaluate whether the difference justifies a claim

- Factor in potential premium increases over the next 3-5 years

Premium increases following a claim can range from 10% to 40% depending on your insurer and claims history. If you're paying $1,500 annually for homeowners insurance and rates increase 20%, that's an extra $300 per year. Over five years, that's $1,500 in additional premiums, potentially wiping out any savings from the claim.

Minor, Localized Repairs

Small issues like a few missing shingles after a windy day or minor flashing repairs typically cost a few hundred dollars. These repairs fall well below most deductibles and don't warrant involving your insurance company.

When you work with a local roofing contractor for these smaller issues, you often get faster service and maintain full control over the process. Our roof repair services focus on fixing what needs attention with clear cost estimates upfront, helping you understand exactly what you're paying for without the uncertainty of an insurance adjustment.

Preventing Claims History Issues

If you've filed claims recently for other reasons, adding a roof claim might trigger non-renewal or significant rate increases. Homeowners who filed a claim within the past two years should carefully weigh whether another claim is worth the risk.

The Claims Process: What Actually Happens

Understanding the insurance claim process helps you decide if you're ready to navigate it. The process involves multiple steps and can take weeks or even months to complete.

Initial Steps After Discovering Damage

- Document everything immediately with photos and videos from multiple angles

- Make temporary repairs to prevent further damage (save receipts)

- Contact your insurance company within the timeframe specified in your policy

- Request a copy of your policy to understand coverage limits and exclusions

- Get independent estimates before the adjuster visits

The question of should i call insurance for roof damage becomes more complex once you understand that the adjuster works for the insurance company, not for you. Their job is to assess damage according to policy terms, which may differ from what you or your contractor believe is necessary.

Working with Adjusters

Insurance adjusters evaluate damage based on strict guidelines and policy language. They determine:

- Whether damage is covered under your policy

- The extent of repairs needed versus full replacement

- Actual Cash Value (ACV) versus Replacement Cost Value (RCV)

- Depreciation factors based on roof age

Many policies pay claims in two stages. First, you receive ACV, which accounts for depreciation. After repairs are complete, you receive the recoverable depreciation to reach the full RCV. This means you'll need to cover costs upfront before receiving full reimbursement.

Special Considerations for Storm Damage

Eastern North Carolina homeowners face unique challenges with hurricane season, tropical storms, and severe coastal weather. These events create specific scenarios where insurance becomes essential.

Wind Damage Documentation

Wind damage can be subtle. Shingles might lift without blowing off entirely, creating vulnerability that leads to leaks months later. After any significant wind event:

- Inspect from the ground with binoculars

- Look for lifted, creased, or missing shingles

- Check for granule loss in gutters

- Examine flashing around chimneys and vents

- Document everything with time-stamped photos

Hail Impact Assessment

Hail damage isn't always immediately visible from the ground. Professional inspectors know what to look for, including:

- Circular bruises or dents in shingles

- Loss of granules exposing the mat

- Cracked or broken shingles

- Damage to metal components like vents and flashing

Reviews.com notes that homeowners should compare the full cost of repairs against their deductible and consider how filing might affect future premiums, especially for older roofs where the payout might be limited by depreciation.

Age of Your Roof Matters Significantly

The age of your roof dramatically affects both coverage and whether filing a claim makes financial sense.

| Roof Age | Typical Coverage | Claim Worth It? |

|---|---|---|

| 0-10 years | Full replacement cost | Usually yes for major damage |

| 10-15 years | RCV with depreciation | Depends on damage extent |

| 15-20 years | Limited RCV or ACV only | Often questionable |

| 20+ years | ACV only, possible exclusions | Rarely beneficial |

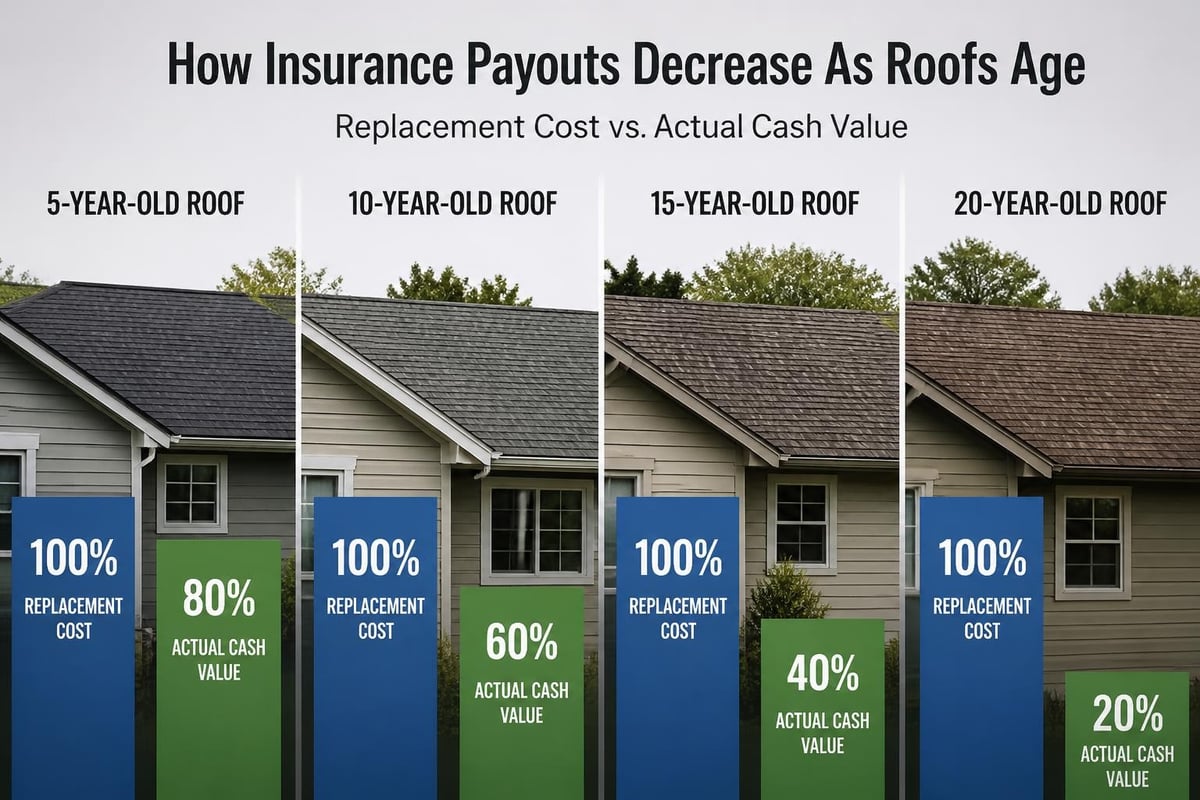

Older roofs receive less coverage because insurers factor in depreciation. A 20-year-old roof might only receive 20-40% of replacement cost, even for covered damage. If you're wondering should i call insurance for roof damage on an aging roof, calculate what you'll actually receive after depreciation before making the call.

Replacement Cost vs. Actual Cash Value

Replacement Cost Value (RCV) pays to replace damaged materials with new materials of similar quality, minus your deductible. This provides the most coverage.

Actual Cash Value (ACV) pays replacement cost minus depreciation based on age and condition. A 15-year-old roof might be depreciated 50-60%, significantly reducing your payout.

Check your policy to understand which type of coverage you have. Some insurers automatically switch older roofs to ACV-only coverage, which makes claims far less valuable to homeowners.

Getting Professional Assessments Before Calling

Before contacting your insurance company, get an independent assessment from a local roofing contractor. This gives you critical information:

- Realistic repair or replacement costs

- Whether damage qualifies as insurance-worthy

- Documentation to support your claim if you file

- Alternative solutions if you choose not to file

A detailed inspection report becomes valuable whether you file a claim or not. If you do file, it provides supporting documentation. If you don't, it gives you a clear scope of work for obtaining competitive repair bids.

Some contractors offer free inspections, while others charge a modest fee that's credited toward repairs if you hire them. Either way, this upfront investment helps you make an informed decision about should i call insurance for roof damage.

Reading Your Policy's Fine Print

Insurance policies contain specific language about roof damage claims that affects your decision. Key sections to review include:

Coverage limitations:

- Age-based restrictions or depreciation schedules

- Coverage caps for roof damage specifically

- Required maintenance provisions

- Exclusions for specific types of damage

Claim requirements:

- Notification timeframes after discovering damage

- Documentation standards

- Requirements for temporary repairs

- Procedures for disagreeing with adjusters

Premium and deductible structure:

- Standard deductible versus wind/hail deductible

- Percentage-based deductibles common in coastal areas

- Claim-free discounts you might lose

Many coastal North Carolina policies include separate wind/hail deductibles that are higher than standard deductibles or calculated as a percentage of your home's insured value. A 2% wind deductible on a $300,000 home means you pay the first $6,000 of wind damage repairs.

Alternative Solutions to Consider

Sometimes the best answer to should i call insurance for roof damage is to explore alternatives that preserve your claims history while addressing necessary repairs.

Payment Plans and Financing

Many roofing contractors offer financing options for larger repairs or replacements. While you'll pay interest, you avoid:

- Claims on your insurance record

- Potential premium increases

- The hassle of the claims process

- Depreciation reductions in payouts

Compare the total cost of financing against your potential insurance payout after deductible and depreciation. You might find the difference is smaller than expected.

Prioritizing Critical Repairs

Not all damage requires immediate comprehensive repairs. A qualified contractor can identify:

- Critical repairs that prevent further damage or leaks

- Important repairs that should happen soon but aren't emergencies

- Cosmetic issues that can wait

Addressing critical repairs out of pocket while postponing less urgent work spreads costs over time and keeps your insurance available for truly catastrophic damage.

Roof Maintenance Programs

Regular maintenance catches small issues before they become insurance-worthy problems. Annual or bi-annual inspections identify:

- Loose or damaged shingles that need replacement

- Flashing that needs resealing

- Debris accumulation causing drainage issues

- Early signs of wear requiring attention

These preventive measures cost far less than major repairs and help you avoid the question of whether to file a claim altogether.

Making Your Decision: A Practical Framework

When you discover roof damage, work through this framework to reach a clear decision:

Step 1: Assess Immediate Safety

- Is there active leaking?

- Is structure compromised?

- Could delay cause additional damage?

Step 2: Document Thoroughly

- Take detailed photos and videos

- Note the date and weather conditions

- Save any physical evidence

Step 3: Get Professional Assessment

- Hire a local contractor for independent evaluation

- Request detailed written estimates

- Ask about repair versus replacement options

Step 4: Calculate True Costs

- Subtract your deductible from repair estimate

- Factor in potential premium increases

- Consider depreciation if roof is older

- Review recent claims history

Step 5: Review Your Policy

- Confirm coverage for this type of damage

- Check age-related limitations

- Verify notification requirements

- Understand your deductible structure

Step 6: Make the Call

- If benefits clearly exceed costs, file the claim

- If costs are marginal, lean toward self-pay

- If uncertain, consult with your agent about hypothetical scenarios

The concept of should i call insurance for roof damage really comes down to whether the financial benefit justifies the long-term cost and whether the damage truly qualifies under your policy terms.

What Happens If You Wait Too Long

Insurance policies include specific timeframes for reporting damage. While these vary by company and state, most require "prompt" or "immediate" notification of losses.

Waiting too long can result in:

- Claim denial based on late reporting

- Increased damage that the insurer argues could have been prevented

- Difficulty proving the damage occurred during a covered event

- Loss of evidence as conditions change over time

However, this doesn't mean you must call within 24 hours of discovering damage. Take time to assess, document, and get estimates. Just don't wait weeks or months hoping the situation improves on its own. Most experts recommend contacting your insurer within a few days to a week of discovering significant damage, even if you haven't made a final decision about filing.

When Insurance Companies Deny Claims

Even when you file a claim for legitimate damage, insurers sometimes deny coverage. Common reasons include:

- Pre-existing damage that wasn't from the reported event

- Wear and tear misidentified as storm damage

- Excluded perils like flood or earthquake without specific riders

- Lack of maintenance that the insurer claims contributed to damage

- Late reporting beyond policy requirements

If your claim is denied and you believe the decision is wrong, you have options:

- Request a detailed explanation in writing

- Get a second opinion from an independent inspector

- Hire a public adjuster to represent your interests

- File an appeal with your insurance company

- Contact your state's insurance commissioner if necessary

Understanding these possibilities before you call helps you prepare documentation that supports your claim and reduces the chance of denial.

Regional Considerations for Coastal North Carolina

Homeowners in Hampstead, Topsail, Surf City, Holly Ridge, and Wilmington face specific insurance challenges related to coastal location.

Hurricane and wind coverage:

Many coastal policies include separate wind deductibles or even exclude wind coverage entirely, requiring separate wind-only policies through the state's Beach Plan. Know what coverage you actually have before assuming storm damage is covered.

Salt air and weathering:

The coastal environment accelerates roof aging, which affects depreciation calculations. Insurance adjusters familiar with coastal properties understand this, but some may not account for accelerated weathering appropriately.

Storm frequency:

Multiple storms in a single season create documentation challenges. If you experience damage from one storm but another follows before repairs are complete, photograph and document each event separately.

Living near the coast means you should review your policy annually and understand exactly what's covered, what your deductibles are, and how roof age affects your coverage. This preparation makes the decision about should i call insurance for roof damage much clearer when the time comes.

Deciding whether to involve your insurance company depends on damage extent, your deductible, potential premium changes, and your roof's age. Getting a professional assessment first gives you the information needed to make a smart choice. NC Roofs provides honest roof inspections and detailed reports that help Hampstead and coastal North Carolina homeowners understand their options before making any commitments about repairs or insurance claims.