Understanding how insurance for roof replacement works can make the difference between paying thousands out of pocket or getting the coverage you deserve. Most homeowners never think about their roof until something goes wrong, and that's often when they discover their policy doesn't work the way they expected. Knowing what your insurance actually covers, how to document damage properly, and when replacement qualifies under your policy helps you make informed decisions when your roof needs attention. This guide walks through the essential details Eastern North Carolina homeowners need to understand about insurance coverage for roofing projects.

What Insurance for Roof Replacement Actually Covers

Homeowners insurance typically covers sudden, unexpected damage rather than gradual wear. Your policy responds to specific perils listed in your coverage, not to aging materials that have simply reached the end of their lifespan.

Covered Perils and Events

Most standard policies cover roof damage from:

- Wind and hail damage from severe storms

- Fire damage including lightning strikes

- Fallen trees or branches that puncture or damage the roof structure

- Vandalism or malicious mischief

- Weight of ice or snow in applicable regions

Wind and fire damage fall under covered perils in nearly all policies, while other events depend on your specific coverage. Eastern North Carolina sees its share of wind events, making this coverage particularly relevant for local homeowners.

What Insurance Doesn't Cover

Understanding exclusions matters just as much as knowing what's covered. Your policy won't pay for:

- Normal wear and tear from aging

- Maintenance issues left unaddressed

- Pre-existing damage from previous storms

- Cosmetic damage that doesn't affect function

- Damage from lack of routine upkeep

The key distinction is sudden versus gradual. A tree falling during a storm is sudden. Shingles deteriorating over fifteen years is gradual. Insurance handles the first scenario, not the second.

How Policy Type Affects Your Roof Coverage

The type of homeowners insurance policy you carry directly impacts what you'll receive when filing a claim for roof damage. Two main approaches determine payout amounts.

Replacement Cost vs. Actual Cash Value

| Coverage Type | What You Receive | Example Payout | Best For |

|---|---|---|---|

| Replacement Cost | Full cost to replace with new materials | $12,000 for new roof | Newer homes, homeowners wanting full protection |

| Actual Cash Value | Replacement cost minus depreciation | $6,000 for 15-year-old roof | Older homes, lower premium seekers |

| Limited Coverage | Depreciated value based on roof age | Varies by age schedule | Older roofs, reduced premiums |

Replacement cost versus actual cash value policies handle claims completely differently. With replacement cost coverage, your insurer pays what it costs today to install a comparable new roof. With actual cash value, they subtract depreciation based on your roof's age and condition.

A ten-year-old architectural shingle roof might have lost 40% of its value through depreciation. Under actual cash value coverage, you'd receive 60% of replacement cost, leaving you to cover the gap.

Age-Based Coverage Limitations

Many insurers now use age thresholds that change how they calculate insurance for roof replacement:

- Roofs under 10 years: Full replacement cost coverage typically available

- Roofs 10-15 years: May require inspection, possible ACV conversion

- Roofs over 15 years: Often limited to actual cash value only

- Roofs over 20 years: May face coverage restrictions or policy non-renewal

Some carriers won't write new policies on homes with roofs over a certain age without replacement first. This affects both new purchases and policy renewals.

Filing a Claim for Roof Replacement

The claims process requires specific steps to document damage and support your request. Missing any of these can slow down approval or reduce your payout.

Immediate Steps After Damage

When you suspect roof damage from a storm or other event:

- Document the date and time of the damaging event

- Take photos and videos from ground level showing visible damage

- Make temporary repairs to prevent further damage (save receipts)

- Contact your insurance company within the timeframe specified in your policy

- Request a professional inspection to assess the full extent of damage

Filing tornado insurance claims requires thorough documentation from the start. The same principles apply to any storm damage claim.

Working with Adjusters

Your insurance company sends an adjuster to evaluate the damage. Understanding this process helps you prepare:

Before the adjuster arrives:

- Gather documentation of your roof's age and previous repairs

- Have photos ready showing pre-storm and post-storm conditions

- Note any interior damage like water stains or leaks

- Prepare questions about your coverage and the claims process

During the inspection:

- Walk through the damage with the adjuster

- Point out all affected areas

- Ask how they're calculating depreciation

- Request a detailed written estimate

- Understand their timeline for decisions

Adjusters evaluate whether damage meets the threshold for replacement or if repairs suffice. They also determine if the damage resulted from a covered peril or existed before the claim event.

Understanding the Estimate

The adjuster's estimate breaks down into specific components. Review it carefully for:

- Scope of work: What repairs or replacement they're approving

- Material specifications: Type and quality of materials included

- Depreciation amount: How much they're withholding initially

- Code upgrade coverage: Whether policy includes bringing roof to current building codes

- Matching coverage: If policy covers replacing the whole roof when only part is damaged

Many policies pay claims in two phases. You receive actual cash value upfront, then recoverable depreciation after completing the work. This protects the insurer while ensuring you actually make the repairs.

Factors That Influence Coverage Decisions

Several variables affect whether insurance for roof replacement gets approved and how much you receive. Some you control, others depend on your policy terms.

Roof Material and Lifespan

Different roofing materials have different expected lifespans, which insurers consider:

| Material | Expected Life | Insurance Preference | Replacement Frequency |

|---|---|---|---|

| Asphalt Shingles | 20-25 years | Standard coverage | Every 20-25 years |

| Architectural Shingles | 25-30 years | Preferred, may get discounts | Every 25-30 years |

| Metal Roofing | 40-70 years | Often discounted premiums | Every 40+ years |

| Tile or Slate | 50-100 years | Premium material, higher coverage | Rarely full replacement |

The material on your roof when you file a claim affects both eligibility and payout calculations. Premium materials often qualify for better coverage terms.

Maintenance History and Proof

Insurers increasingly request maintenance records. Regular upkeep demonstrates responsible ownership and supports your claim. Keep records of:

- Annual inspections by qualified contractors

- Repairs made between major weather events

- Cleaning and maintenance work

- Previous insurance claims and resolutions

Homes in Eastern North Carolina benefit from documented roof repair history, especially after hurricane season when multiple storms may cause cumulative damage over months or years.

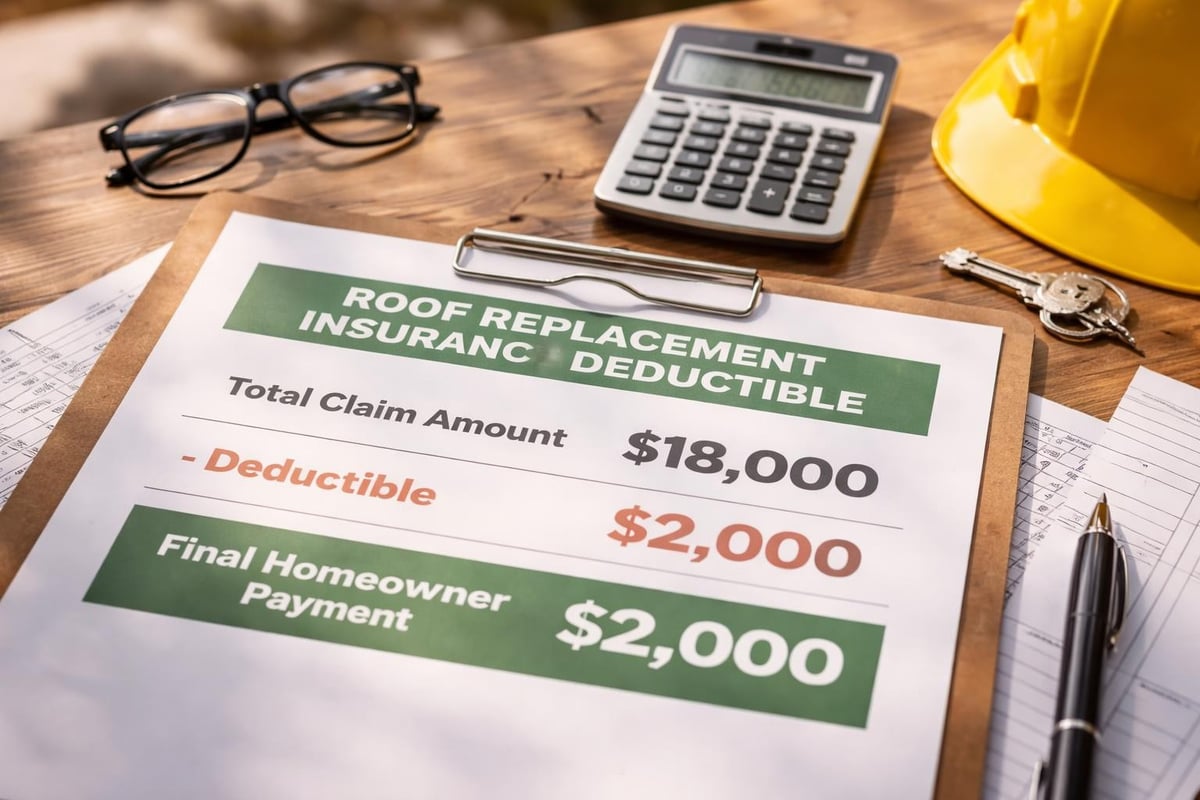

Deductibles and Out-of-Pocket Costs

Your deductible directly impacts what you pay versus what insurance covers. Common deductible structures include:

Flat deductibles: Fixed dollar amount ($1,000, $2,500, $5,000)

Percentage deductibles: Percentage of home's insured value (1%, 2%, 5%)

Wind/hail deductibles: Separate, higher deductible for wind and hail damage specifically

A home insured for $300,000 with a 2% wind deductible means you pay the first $6,000 of wind damage claims. On a $15,000 roof replacement, you'd receive $9,000 from insurance.

Regional Considerations for Eastern North Carolina

Location affects both coverage availability and claim frequency. Eastern North Carolina's climate presents specific insurance challenges for roofing.

Hurricane and Wind Coverage

Coastal and near-coastal areas face higher premiums and specialized wind deductibles. After major hurricanes, some insurers:

- Increase deductibles on renewed policies

- Add waiting periods for new wind coverage

- Require separate windstorm policies through state pools

- Limit coverage on older roofs more strictly

Understanding roof coverage options becomes critical when you live in storm-prone regions where wind damage drives most roof insurance claims.

Multiple Storm Events

When several storms pass through in one season, distinguishing which event caused which damage complicates claims. Insurers may:

- Attribute damage to the first reported event only

- Require separate claims for each storm

- Dispute whether new damage occurred or pre-existing damage worsened

Documenting your roof's condition between weather events protects you. Photos after each storm create a timeline showing when specific damage appeared.

Making Smart Decisions About Coverage

Choosing the right insurance for roof replacement coverage requires balancing premium costs against potential claim scenarios. Consider these factors when evaluating your policy.

When to Consider Replacement Cost Coverage

Pay the higher premium for replacement cost coverage if:

- Your roof is relatively new (under 10 years old)

- You plan to stay in the home long-term

- Your budget couldn't absorb a major replacement cost

- You live in an area with frequent severe weather

- Your roof uses premium materials like metal or tile

The premium difference between actual cash value and replacement cost typically runs $100-300 annually. That's often worth it for full coverage.

When Actual Cash Value Makes Sense

Actual cash value coverage might work if:

- Your roof is already 15+ years old

- You're planning to replace the roof soon anyway

- You have substantial emergency savings

- You're selling the home within a few years

- You're primarily concerned with catastrophic loss, not routine damage

Some homeowners intentionally choose ACV coverage on older roofs, knowing they'll replace soon regardless of insurance claims.

Questions to Ask Your Insurance Agent

Get clarity on your specific policy by asking:

- Is my roof coverage replacement cost or actual cash value?

- What specific perils does my policy cover for roof damage?

- Do I have any special deductibles for wind or hail?

- How does my roof's age affect my coverage?

- Does my policy include code upgrade coverage?

- What documentation do I need to support a roof claim?

- Are there any coverage limitations based on roof material?

- How does depreciation get calculated on my policy?

Understanding homeowners insurance and roofs means knowing exactly what you're paying for before you need to file a claim.

Working with Contractors During Insurance Claims

The contractor you choose affects your claim outcome. Insurance companies have requirements, and selecting the right roofing company matters.

Getting Multiple Estimates

Most insurers don't require multiple estimates, but getting them helps:

- Verify the adjuster's estimate is reasonable

- Understand the full scope of needed work

- Compare different repair versus replacement approaches

- Ensure you're not leaving covered damage unaddressed

Reputable contractors provide detailed estimates breaking down materials, labor, and specific work items. This transparency helps when discussing coverage with your insurer.

Avoiding Insurance Fraud Schemes

Some contractors engage in practices that constitute fraud:

- Offering to waive your deductible (illegal in most states)

- Promising to "handle everything" with your insurance

- Inflating damage estimates to increase claim amounts

- Performing work not approved by your insurer

- Pressuring you to sign contracts before the adjuster visits

Legitimate roofing companies work within insurance guidelines while advocating for complete and fair coverage of actual damage.

Understanding Insurance-Ready Documentation

Professional contractors provide documentation that supports claims:

- Detailed inspection reports noting all damage

- Photos with measurements and specific locations

- Comparisons to building code requirements

- Material specifications matching your policy

- Clear estimates separating covered from non-covered work

This documentation helps adjusters understand the full scope and supports your claim for comprehensive repairs or replacement when warranted. For Eastern North Carolina homeowners, working with contractors who understand regional weather patterns and common storm damage creates stronger claim documentation.

What to Expect After Claim Approval

Once your insurance for roof replacement claim gets approved, the work begins. Understanding the payment process and completion requirements protects you.

Claim Payment Structure

Insurance companies typically structure payments in phases:

Initial payment: Actual cash value (replacement cost minus depreciation)

Held back: Recoverable depreciation

Final payment: Released upon proof of completed work

You'll need to submit final invoices, photos of completed work, and sometimes a completion certificate before receiving the held-back depreciation. This ensures the money actually goes toward the approved repairs.

Completion Requirements

To receive full payment, document:

- Signed contract with the roofing contractor

- Proof of permits pulled and inspections passed

- Before and after photos

- Paid invoices showing work completion

- Any required warranties or guarantees

Missing any of these can delay your final payment by weeks or months. Keep organized records throughout the project.

Understanding insurance for roof replacement helps Eastern North Carolina homeowners navigate claims confidently and get the coverage their policies provide. The key is knowing your policy terms, documenting damage thoroughly, and working with professionals who understand both roofing and insurance processes. When you need honest guidance on roof condition and insurance-ready documentation, NC Roofs provides clear assessments and straightforward recommendations to help you make the best decision for your home and budget.